The experience of co-buying a home with 8 people

Exciting, stressful, brutal, mysterious, huge… All these words are frequently used to describe the process of buying a first home. Now, take that massive process, and add more people to multiply the stress, excitement and chaos. I co-bought a home recently, with a group of eight. This is the story of what it was like.

We set the pace with many long, draining meetings that went well into the night. Then out of the blue, we did an impulse buy, offering to buy a house on the night that we viewed it. All in all it took us around 8 months, from looking at the first house to finally buying one together.

Like us, you might be looking for solutions to a highly priced property market that has locked you out. You might be looking for a way to move into home ownership but keeping on living together with your friends. Maybe you’re fascinated at the idea of 8 people buying a house together. Or you might be a group process nerd, wondering how people make decisions together when it’s the biggest purchase of their life. Well, read on! It’s all in here.

The birth of our home-buying dream

I first met my partner Jody at a house called the “Treehouse”, a beautiful wooden home high up on the Southern hills of Wellington. Jody lived at the Treehouse with an awesome community. This was a group of people that ate together, made music together, had adventures together, and shared more than a few hard times too. They were all around 30 — a little old for renting, by traditional baby boomer standards. But they loved living together, and renting was the way to do it.

We all got together for a tramp (hike) last year, and that’s where the conversation started. Charlotte, one of our group, was planting the seed, seeing who was interested in home co-ownership. It seemed like a logical next step for us — most of us already lived together, why not take the next step and buy our next house together?

Plus, we’d all heard about housing crises, increasing social isolation, and increasing inequality in the distribution of property wealth. Here was an opportunity to take one small step in a different direction.

On paper, it looked pretty good. We could buy a million dollar home between 4 couples, and pay only $250k per couple. Under half the cost of one couple buying a house on their own in Wellington at that time. And saving a deposit is much easier for a $250k bank loan than a $600k loan!

But it wasn’t just about numbers on paper. Buying a house meant that we could keep living together. It’s normal for folks in New Zealand to rent a house together with some friends, as their first step after leaving home. Over time, most people will drift away from their shared living arrangements, to move into a place by themselves — especially if they buy their own house. Some people love this kind of quiet life, but it wasn’t for us. We wanted to have our cake and eat it too. Buy our own house, but keep doing shared living.

So we started talking about the idea more and more, getting excited. I shared the dream with friends and family. I said to them, “I want to buy a house with 8 people!” Common responses included:

- What? Why?

- Sounds like a cult!

- You are clearly all a bunch of weirdos and I would never do what you are doing, but you seem excited, so good for you.

- Good on ya, that’s a creative way to get on the property ladder.

- Wow, what an amazing idea! I wish I could live in a community.

- Are you on Loomio yet?

It was time for the excitement to turn into something. We started an online group chat, invited everyone, and we were away!

Our first fling

We started by looking at a huge old house by the sea. 7 bedrooms and counting, built 100 years ago. Boy did this place have history. We heard it had been used as a World War II bunk house, and as a brothel. It was beautiful and we loved it! That was when our first serious group chats began.

And when I say serious, I mean serious. I was pretty green, didn’t really know much about owning a home or buying a home. And now we were jumping into conversations about home insurability, costs of roofing upgrades, and where we would fit in our music room. It was a bit jarring. Kind of like discussing what colour your baby room will be, on your second date.

That was when I realised how lucky I was to be part of a group that had lots of different expertise. We had building/construction knowledge, geology knowledge, legal skills, facilitation skills, financial skills, risk mitigation skills. We all saw things that the others in the group didn’t. All our bases covered — great!

Learning #1. You can access a lot more expertise when you buy a house in a group.

With so many perspectives in the room, we had MAMMOTH conversations. It wasn’t just expertise, skills and perspectives to exchange. It was uncovering our individual needs, figuring out how to align with each other, and just basically building relationships. And while all that information was flying around, we were also figuring out our process for making really big decisions as a group. It was overwhelming.

Needless to say, we didn’t come close to getting that first house. We spent most of our energy on dreaming about our new life together, and trying to resolve the differences between everyone’s dreams. It took time and energy away from other important conversations, such as agreeing on how much we could realistically afford to spend, or what was a sensible amount to offer for the house. Knowing people’s dreams was actually really great, but all the back and forth took a toll on us.

It took so long, that we were looking at multiple other options on the market while this agreement process was slowly working through its twists and turns. We were splitting our attention, our momentum was cooling off, and eventually we hit a bump in the road.

Learning #2. Share your dreams with the group, but not the specifics. You could spend a very long time arguing about the details.

A bump in the road

Things came to a halt. My partner Jody and I thought we were no longer in a financial position to buy, so we couldn’t commit to pursuing any houses. The rest of the team turned their attention to finding an awesome place to rent together, and continuing to check out a few houses just for research. For a moment, our home co-ownership dream was de-prioritised, in danger of quietly slipping away. All that conversation time and effort we invested, and we hadn’t even made an offer on one home yet!

Things went quiet. A month or so passed.

The group found a home they loved for sale, and longingly watched the closing date pass by, since we couldn’t buy anything yet. But wait! The closing date passed, and this new house hadn’t been sold! There was a chance we could buy it if we were quick. Suddenly excitement was in the air again. Jody and I were looking around frantically for financial back up plans… yes! There’s a way it could work! As a group, we had clawed our way back in to the property market.

Learning #3. Don’t give up when the group starts drifting. Give it some time, and when excitement pops up again, even impossible roadblocks can be moved.

Getting back into the dating scene

After a bit of a break, we’d somehow found ourselves back in the scene. It was a whirlwind romance — we could only buy this house if we were quick. We rushed around, knowing time was running out. Talking to banks, getting all the documentation they needed… Oh no! We just heard news the house had sold before we could get our affairs in order.

It was sad, but we still had a lot of momentum behind us. We were as close as we’d ever been to buying something. Our group’s dream was coming back into focus. It was time to take the next step, and find some legal advice from someone who wasn’t in our home buying group.

By this point, we had gained some confidence. We’d looked at many houses, talked the talk to real estate agents, and understood the whole process much more than we did at the start. We’d been through some bumps, but we’d gotten closer than ever.

A trip to our new solicitor showed us how much we didn’t know. Suddenly a whole new world was opening up: making wills, getting life insurance, being liable to each other, mortgage protection insurance, owning as ‘tenants in common’ or forming a trust to buy the house… my head was spinning. But at least now I was aware of what I didn’t know, as opposed to living in blissful ignorance.

While this felt like a bit like a step back, it really was a level-up for the group.

Learning #4. Find some good advice! Even though it can hurt to admit it, known unknowns are much better than unknown unknowns.

Playing games with commitment

Another interesting home had popped up on the market. It had lots going for it, but lots of things weren’t quite right too. After long deliberations, we decided to go ahead with low commitment, and offer a low amount for the house. If our offer was accepted, then we would have a pretty great place to live for a bargain! If our offer wasn’t accepted, then no harm done — we weren’t particularly invested anyway.

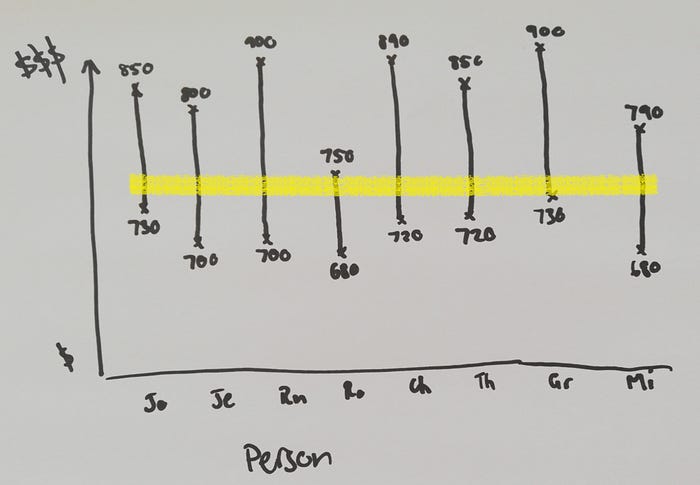

We needed to put a number on it now, and for that we used a group process. We asked each person two questions:

- What is your maximum — the most money you’d be willing to pay for this house as as group?

- What is your minimum — where’s the point that you think the offer amount is too small to even bother?

We ended up with something like the below diagram:

Luckily, there were some numbers in the middle that were between everyone’s minimums and maximums. This was our group’s comfort zone (highlighted in yellow above). Picking a number from within that collective comfort zone was then quite an easy job! In the end, we offered something like $740,000.

Unfortunately, our low commitment strategy left us without a home, which was hardly surprising in a time when it was much easier to sell houses than it was to buy them. We later found out the home had sold for $801,000; $60,000 more than what we were willing to pay. But we’d crossed an important milestone. We’d found a way to agree on an amount to pay. And we’d formalised that amount by signing an offer together. It was a nervous offer, but an offer nonetheless.

Learning #5. When it’s hard to agree on a number, and you want everyone to feel comfortable, ask people for a range (or “comfort zone”).

Our first true love

Just like that, something very special popped up on our radar. We’d shared our dreams, we’d come through bumps in the road, and we’d toyed with commitment. We were finally ready to fall in love. And this was our house to fall in love with. Many of the homes we’d seen had been watered down, made to look sensible, something to appeal to the masses. This one was different. It had real personality, and it wasn’t even trying to hide it.

We were captivated.

It was amazing to find a property that all eight of us loved. And it turns out that being in love set us up for a lot of challenge. Emotions were running high, there was more at stake. We were dealing with real fear now, the fear that another home buyer would offer more than us, and our dream home would disappear. Some of us felt the need to offer a lot of money, to safeguard against losing our dream. Others feared paying too much, signing up for big mortgage repayments which would hurt their quality of life. Our fears and needs suddenly had sharper edges, and they were coming into direct conflict.

To add to the challenges, one of our group was in China for work. He was trying to participate in all the discussions remotely, and he’d only seen the house we were talking about via video call. We’d never practiced having remote meetings before, and we weren’t very good at it. Our technology sucked for remote participation, and our process wasn’t very good for it either.

With these challenges all stacking up, we pushed each other more than we ever had. Our meetings went later into the night, and there were tears on more than one occasion. In this highly charged atmosphere, we knew we needed extra safeguards when we were deciding how much money we were going to offer for our beloved new home.

So we added an extra step to our “group comfort zone” process, to convert it from everyone’s comfortable to everyone explicitly agrees. As before, we outlined our minimum and maximum $$$ amounts, and found the range that everyone was comfortable with. Then our extra step was a bit of maths. Each person wrote down their preferred offer amount, down to the last dollar. We took each person’s number, and calculated an average. Lo and behold! This average figure happened to fit within the group’s comfort zone. So not only we were comfortable, we also had a sense of mathematical fairness. That fairness enabled us to explicitly agree on how much we offered as a group.

Getting down on one knee

We had figured out our price, and it was a generous one — $956,000 for a home valued at $760,000. We’d signed the paper, and we were ready to make our big proposal. We all went in to the real estate agent’s office to present her with the paperwork, and from there, it was in her hands. Imagine getting down on one knee and asking someone to marry you, and hearing them say back: I’ll think about it, let me just check if I have any better offers. We could only wait. And wait. It was a real nail-biter.

I still remember the day. I was at work, I could barely focus on anything. Every five minutes, I was checking my phone to see if we had news. Seconds dragged into minutes which dragged into hours. Silence. By the end of the day, all we’d heard was that they needed more time.

The next day, we all heard the thing we feared most. Our dream home had gone to somebody else.

This news was very hard for our group to handle. After all this time, we’d finally allowed ourselves to fall in love. And we’d been rejected. To be honest, given we were offering nearly $200,000 more than the value of the home, I was quite shocked to hear we hadn’t been successful. It was a demoralising moment. If we couldn’t buy a house with that kind of offer, how were we ever going to get anything?

Later, I had a disturbing thought. We may well have offered the highest $$$ amount. But the house seller probably didn’t want it, because we’d included a bunch of conditions with that amount. The seller would have preferred the absolute certainty of having no conditions, so someone else walked away with our dream home, even though they quite possibly offered less money than we were willing to pay.

The worst part about it? We only included conditions, because we didn’t know any better. I learned later that it’s totally possible to make a condition-less offer, what people call a “clean offer”. If I’d only known what I know now, I’m quite certain that we could have been successful.

To add insult to injury, this was around the time when our bills started to hit — paying our solicitor, builder’s reports, etc. It was a lot more expensive than we thought it would be, and it really felt like we’d just thrown a lot of money away for nothing.

Learning #6. If it’s a seller’s market, don’t lose your dream home to unnecessary finance conditions. Find out how you can make a clean offer that is simple to say yes to. See the appendix at the end for some advice on making clean offers!

On the rebound

After our rejection, our home buying group was low on hope. I felt like we‘d never find another house again that we all loved. It was just so hard to muster any excitement about anything. I started hearing our group say things like “I need to check out of this process for a while”, “we’ve taken too many beatings this week”, and “we need to spend some time together that isn’t talking about houses”.

Against this backdrop, we found a place that looked OK on paper, but didn’t rev any of our engines. I wanted us to go for it — less out of desire for the house, more out of fear that we would completely fade away if we didn’t keep up some forward motion. Because there was so little collective energy, I asked one of the others to step into the driving seat with me. We took the reins for most things, but returned back to the group for the big decisions.

Having one or two drivers actually turned out to be quite an effective strategy. It protected our collective from decision fatigue at a point of low energy. This strategy wouldn’t have worked if it was a house that the whole group loved. It worked because this house was low stakes for us. We weren’t ready to fall in love again, but we sure were ready for a low commitment rebound.

Our rebound represented our strangest group process so far. We almost forgot about the house until right at the last minute. I used a random number generator to figure out our $1,086,628 offer price — well under the $1.27 million valuation. I was the only one who signed the piece of paper that made our offer legally binding. It felt very strange to do it this way, after having big group conversations where we discussed every little detail together. This time, I said to the group, I propose we make an offer of just under $1.1 million, with abc conditions, and xyz other details. Can I hear a ‘yes’ or ‘no’ from each of you. Very little collaboration, except for asking for consent at the end.

Our rebound didn’t work out either, because our offer amount was too low. This didn’t really matter. The important thing was that we maintained our forward momentum, and while doing that we successfully trialled another group decision making process.

Learning #7. Buying a house together is a high stakes commitment, but it doesn’t need to mean constant decision fatigue for everyone in the group. One -person or two-person proposals are great for any decisions with lower stakes.

Our Vegas speed wedding

The strangeness and surprises weren’t done yet. We were right at the end of 2019, and had pretty much resigned ourselves to not finding anything until 2020. But there was one last place to look at. One last place, and two days left in 2019 before everything shut down and everyone went on holiday. Time to take a ride on our fastest rollercoaster yet.

It was Wednesday. Some of us had viewed a house, and got pretty excited. We had a video call that night, and decided to make an offer. I hadn’t seen the house yet, and neither had another person in the group. We disagreed a lot on the $890,000 offer amount, and not everyone was happy. In fact this was probably the least agreement we’d ever had on an offer. But time was of the essence, so we let ourselves be pushed outside our comfort zone.

Thursday. We got news that our offer had been accepted. We couldn’t quite believe it. But there was no time to think. Our one mission became: get finance and paperwork sorted by tomorrow, so this offer goes through. We rushed around getting everyone’s signatures on lots of pieces of paper, and got everything signed off just before close of business for the day. This included getting signatures from one of our group in Australia who didn’t have reliable internet access. It was hectic!

Friday. Jody (my partner) and I got cold feet. I was ready to throw in the towel. We teetered back and forth, knowing that we could still block the process from going ahead if we wanted to. Eventually we figured out a way to continue. We were shaky, but we gave our thumbs up.

At 3pm on Friday, two hours before everything was due to shut down for the year, we heard the news. We had “gone unconditional” on the house — it was pretty much a sure thing. Our Vegas speed wedding had been consummated! We’d got it all wrapped up, 48 hours after viewing the house for the first time.

And I hadn’t even seen the house yet in the flesh. Make that a Vegas speed blindfold wedding.

This part of the story has a lot of shakiness, doubt and disagreement. It might look like a breakdown of our group decision process, because we rushed too fast through something uncomfortable, in order to meet unforgiving time constraints. That is somewhat true.

AND, the only thing that got us through that discomfort was having high levels of trust in each other. Personally, I was further outside my comfort zone than before, but in the end I could still trust that the group was making a decision that would work out well for all of us.

Happily ever after?

Suddenly, it was all over. Our first fling, our return to the dating scene, our fears of commitment, our first true love, rejection, our unsuccessful rebound, and finally our speed wedding. All done, just in time for the end of year holiday.

I’m still not quite sure how this sold sign happened. But I do know that our group could have never bought a house this way eight months ago. Time changed us. We built trust, we got to know each other. Our comfort zones evolved. We learned to push each other. Which brings me to the final key learning.

Learning #8. Don’t expect to draw up unanimous, unchanging group agreements straight away. Groups evolve fast. Trust that group alignment gets easier and easier over time, as you trust each other more.

Eight people, eight months, eight learnings. This is how my story ends, the story of eight people taking their first step into home co-ownership. There’s much more to come —moving in, co-ownership agreements to draw up, renovations to organise, community to build. But for now, we know that so much is possible.

It’s possible to beat a tough property market, by buying a house with your friends.

It’s possible to keep living with your friends or housemates, even when you jump from renting to buying a house.

And as for making the biggest financial decision of your life so far? It’s possible to build enough trust to make that decision together.

You might like to take a look at our co-ownership agreement: Link to co-ownership agreement template

Thanks to my friends who bought this house with me, making this whole experience possible:

Jody Burrell, Charlotte Shade, Rosie Sievers, Jesse Kearse, Mike Robinson, Thom Mellor, and Gráinne Patterson

And a big thanks to Clare Stanley, our solicitor who helped us through the whole process.

Written by Rupert Snook

Appendix: making a “clean offer”

At the time we were buying, in Wellington New Zealand during 2019, houses were a scarce resouce. There were lots of people wanting to buy houses, and that meant a big advantage for anyone selling a house. In these market conditions, a seller can afford to be choosy — they will have multiple offers to choose from, so they will pick the offer they like the best. And the most likeable offer isn’t always the highest number. Sometimes it’s the “cleanest” offer, the offer that means more certainty and less hassle for the seller.

The key word here is conditions. Here are the two finance conditions that we included on many of our house purchase offers:

- Your offer will only go ahead if you can get your bank to agree to loan you the money.

- Your offer will only go ahead if your KiwiSaver / pension scheme provider allows you to take out your first home withdrawal.

These conditions are there for your protection. But if the seller sees conditions on your offer, it introduces uncertainty and hassle for them. They might accept your offer, but then you find out your bank won’t agree to lend you the money to buy the house. The seller might have already waited a couple of weeks to receive this news from you, and then they’ll have to go back to their other interested buyers, assuming the buyers haven’t moved on to offer on another house.

Now imagine the seller has another offer on the table. That offer might be $10,000 less than what you’ve offered, but there are no conditions. If the seller accepts that offer, then their house is sold — done and dusted. They had to take a bit less money, but they could sleep easy at night knowing everything was wrapped up. Compare that to the nervy scenario where they accept your offer, and maybe make more money, but they’re taking a gamble.

So, if you find yourself in a “seller’s market”, meaning house sellers can easily pick and choose which offers they accept, then it’s worth making clean offers if you can. I’ll explain the two actions that you can take, if you’re in similar market conditions and similar geography to us.

Firstly, get pre-approval from your bank. We gave the bank our financial information, and they agreed to lend us up to $1.2 million for a home. Then, for any home we were seriously considering, we would send them information about that particular home, and ask them to pre-approve our offer price. That meant our bank could give us a guarantee: if you buy this house for this much money, then we’ll give you the loan. So we had certainty, and this certainty made our offers more attractive. If you can get a letter of pre-approval from your bank too, then you can probably remove the bank loan condition from your offer.

Secondly, go as far as you can with applying for your KiwiSaver first home withdrawal. Some KiwiSaver providers will only give you a pre-approval letter, stating the amount you can withdraw. Other providers will let you go through the full application process, but hold your funds until you can provide a signed Sale & Purchase agreement. Go through the full application process if you can, because this will give you full certainty, and you can start removing KiwiSaver withdrawal conditions from your offer.